The Basics of S Corps for Business Owners: A Physician’s Beginner Guide

In a nutshell: If you’re a physician running your own practice or doing locum work, an S Corp can lower your self-employment tax bill by splitting your income into a “reasonable salary” plus distributions. You only pay payroll taxes on the salary portion. It’s not magic, and it’s not for everyone, but for high-earning doctors, the savings can be real, often five figures a year. You’ll need to file Form 2553 with the IRS, run actual payroll, and stay on top of compliance. Common deductions like retirement contributions, health insurance, and home office expenses still apply, sometimes in better ways.

Understanding the basics of S Corps is essential for physicians considering this business structure.

Now let’s get into it.

What Is an S Corp, Really?

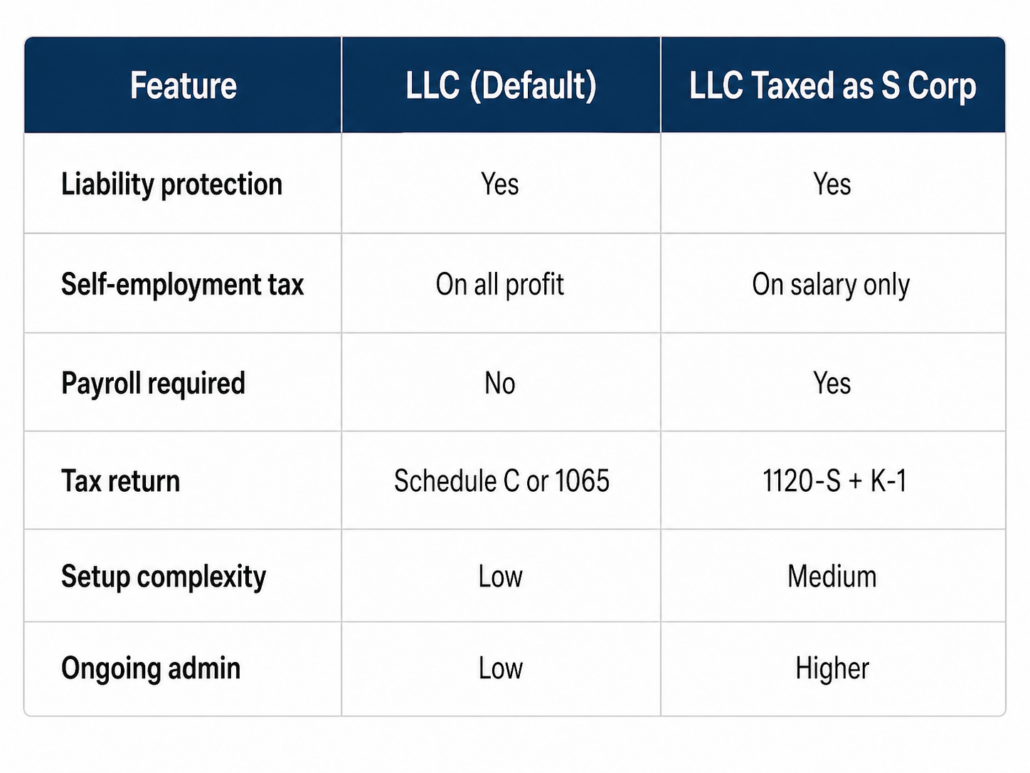

An S Corp isn’t a type of business you “form” from scratch. It’s a tax election. You start with an LLC or a regular corporation, then you tell the IRS you want it taxed as an S Corp by filing Form 2553. That’s the whole trick.

The “S” comes from Subchapter S of the tax code. Boring name, useful structure.

Here’s what makes it different from a regular sole proprietorship or single-member LLC:

- Your business income passes through to your personal tax return, so you avoid the double taxation thing C Corps deal with

- You can split your earnings into salary and distributions

- Only the salary portion gets hit with payroll taxes (Social Security and Medicare)

- The distribution portion skips those payroll taxes entirely

That last point is where the savings live. For a physician pulling in $400,000 from a side practice or locums work, the difference between paying self-employment tax on the full amount versus just on a reasonable salary can be substantial.

I think this is where most doctors get curious, and rightfully so. Self-employment tax is 15.3% up to the Social Security wage base, then 2.9% Medicare after that, plus an extra 0.9% Additional Medicare Tax once you cross certain thresholds. It adds up fast.

The Beginner Version

Imagine you’re a dermatologist doing $300,000 a year through your own LLC, currently taxed as a sole proprietor. You’re paying self-employment tax on basically all of it (minus the deduction for half of it).

Switch to S Corp status, pay yourself a $180,000 salary (which the IRS would likely consider reasonable for a derm), and take the remaining $120,000 as distributions. You only pay payroll taxes on the $180,000. The $120,000 is still taxed as income, but no FICA.

Rough math? You could save somewhere in the ballpark of $4,000 to $8,000 a year, sometimes more. Your actual number depends on a lot of variables, which is why Physician Tax Planning matters and shouldn’t be a guessing game.

How an S Corp Actually Works for Physicians

Let’s get practical. Here’s the flow:

- You set up an LLC or corporation (most physicians go LLC because it’s simpler)

- You file Form 2553 to elect S Corp status (deadlines matter here)

- You set up payroll, usually through a service like Gusto or ADP

- You pay yourself a reasonable salary via W-2

- You take additional profits as distributions

- The business files Form 1120-S each year

- You get a K-1 showing your share of the pass-through income

Sounds like a lot. It is, kind of. But once it’s set up, most of it runs on autopilot.

What Counts as a “Reasonable Salary”?

This is where physicians often trip up. The IRS doesn’t give you a specific number. They just say it has to be “reasonable” for the work you’re doing.

For doctors, reasonable usually means looking at what a similar physician would earn as an employee doing the same work. So if you’re a hospitalist and the going W-2 rate is around $280,000, you can’t pay yourself $80,000 and call the rest distributions. The IRS will notice. They’ve been getting better at noticing, actually.

A few things that influence what’s reasonable:

- Your specialty (a neurosurgeon’s reasonable salary is way different from a family doc’s)

- Your geographic area

- Your hours and patient volume

- What other physicians at your level earn in similar roles

- Industry benchmarks like MGMA data

Most working with a Physician Tax Advisor end up with documentation backing up their salary number. It’s not the kind of thing you want to wing.

Similarities to a C Corp (and Why They Matter)

S Corps and C Corps share some structural stuff. Both require:

- Articles of incorporation (or organization for LLCs electing S status)

- A board of directors or managers

- Annual meetings and minutes (yes, even if you’re the only owner)

- Separate business bank accounts

- Proper bookkeeping

The big difference is taxation. C Corps pay corporate tax, then shareholders pay tax again on dividends. S Corps skip that. For a physician owner-operator, the S Corp almost always makes more sense than a C Corp, though there are edge cases where C Corps win, mainly around fringe benefits and reinvested earnings.

IRS Requirements You Can’t Ignore

To qualify for S Corp status, your business has to meet some rules:

- Be a domestic entity

- Have only allowable shareholders (individuals, certain trusts and estates)

- Have no more than 100 shareholders

- Have only one class of stock

- Not be an ineligible corporation (insurance companies, certain financial institutions)

For most physicians, these are non-issues. You’re usually the sole owner, maybe with a spouse, and you’re operating domestically. Easy.

The Tax Strategy Part: Where Physicians Save Real Money

This is the section most doctors actually care about. Setting up the entity is just plumbing. The savings come from how you use it.

1. The Salary/Distribution Split

Already covered, but worth repeating because it’s the headline benefit. The lower your salary (within reason), the less FICA you pay. The catch: lowball it and you risk an audit.

A good Physician Tax Strategist will run the numbers each year and adjust. What was reasonable when you were doing 30 hours a week of telemedicine isn’t the same once you’ve added in-person clinic days.

2. Retirement Contributions Done Right

S Corps open up some powerful retirement options. The salary you pay yourself is what counts as “compensation” for retirement plan contribution limits.

Common setups for physician S Corp owners:

- Solo 401(k): You can contribute as both employee and employer. Employee side is up to $23,500 in 2025 (over $30,000 if you’re 50+). Employer side adds up to 25% of your W-2 wages.

- SEP-IRA: Simpler, but the contribution limit is based purely on your salary, so it can actually be less generous than a Solo 401(k) for S Corps.

- Defined Benefit Plan: For high earners over 45 or so, this can let you stash $200,000+ a year pre-tax. Complicated, but powerful.

Here’s the thing, your salary needs to be high enough to support the contributions you want to make. So there’s a balance. Pay yourself too little to dodge FICA, and you cap your retirement savings. This tension is real, and it’s why Physician Tax Solutions aren’t one-size-fits-all.

3. Health Insurance Premiums

If your S Corp pays your health insurance premiums and includes them in your W-2 wages (Box 1, not Box 3 or 5), you can deduct them above-the-line on your personal return as self-employed health insurance.

It’s a weird little dance. The S Corp deducts it as wages, you don’t pay FICA on it, and you deduct it again personally. Net effect: the premium is essentially deductible without payroll taxes.

This includes:

- Medical insurance for you, your spouse, and dependents

- Dental and vision premiums

- Long-term care insurance (within limits)

4. The Home Office and Accountable Plan Setup

If you use part of your home regularly and exclusively for business, an S Corp owner can’t take the home office deduction the same way a sole proprietor does. Instead, you set up an “accountable plan.”

The S Corp reimburses you for:

- A portion of your mortgage interest or rent

- Utilities

- Internet

- Home office depreciation (or simplified method)

- Cell phone (business use percentage)

The reimbursement isn’t taxable to you. It’s deductible to the corporation. Clean and simple, if you set it up right.

I’ve seen physicians skip this because it sounds tedious. It’s worth doing. A few thousand a year in legitimate reimbursements adds up over a decade.

5. Other Deductions Worth Knowing

A quick list of things that often get missed or underused:

- CME expenses (conferences, courses, books, subscriptions)

- Medical licensing and DEA registration fees

- Malpractice insurance premiums

- Professional society dues

- Business mileage (track it, the IRS loves documentation)

- Cell phone and tech equipment

- Business meals (50% deductible in most cases)

- Continuing education travel

- Scrubs and specialized work attire (with caveats)

Each of these is small on its own. Stack them, and you’re looking at meaningful savings.

When an S Corp Doesn’t Make Sense

I’d be doing you a disservice if I made it sound like every physician should rush to elect S Corp status tomorrow. Some situations where it’s not the best fit:

- You’re a W-2 employee with no side income (then this isn’t really for you anyway)

- Your self-employment income is under maybe $40,000 to $50,000 (the admin costs eat the savings)

- You’re in a state with high S Corp fees or franchise taxes (California’s $800 minimum, for example, plus 1.5% S Corp tax)

- You’re planning to grow rapidly and take outside investment (S Corps have shareholder restrictions)

- Your income is from passive sources rather than active work

Also, S Corp setup adds complexity. You’re now running payroll, filing a separate return, possibly dealing with state-level S Corp taxes, and keeping more meticulous records. The compliance load is real.

For physicians earning $200,000+ in self-employment income, the math usually works out in favor of the S Corp. Below that, it’s a closer call.

S Corp vs LLC: A Quick Untangling

This confuses people. An LLC is a legal structure. An S Corp is a tax classification. You can have an LLC taxed as an S Corp. They’re not opposites.

For most physicians, the right answer is “form an LLC for liability protection, then elect S Corp status when income justifies it.” The two work together, they’re not either/or.

A Real-World Physician Example

Dr. Patel is a 38-year-old anesthesiologist doing locums work alongside a part-time hospital position. Her locums income is around $250,000 a year through her single-member LLC.

As a sole prop, she’d pay self-employment tax on roughly all of it. Maybe $24,000 in SE tax give or take.

With S Corp election, she pays herself a $160,000 salary (defensible for an anesthesiologist working part-time locums) and takes $90,000 as distributions. Her FICA exposure drops to just the salary portion. Estimated savings on payroll taxes alone: somewhere around $5,500 to $7,000 a year, depending on how the wage base shakes out.

Add in the accountable plan reimbursements for her home office, better-structured retirement contributions, and properly handled health insurance, and her total tax savings climb higher.

Set up costs and ongoing payroll fees? Maybe $2,000 to $3,000 a year all in. Net win, clearly.

The Compliance Stuff Nobody Wants to Talk About

Quick rundown of what running an S Corp actually requires year-round:

- Run payroll on a regular schedule (monthly works for most solo physician owners)

- File quarterly payroll tax returns (Form 941)

- File annual unemployment returns (Form 940)

- Issue yourself a W-2 each January

- File Form 1120-S by March 15

- Keep clean books, ideally in something like QuickBooks

- Hold annual meetings and document them

- Maintain separate business banking

- Track distributions vs salary clearly

Skip these and you risk losing S Corp status, getting reclassified by the IRS, or both. It happens more than you’d think with DIY setups.

Bringing It Together

An S Corp isn’t a silver bullet. It’s a tool. For physicians earning meaningful self-employment income, it’s often a good tool. The savings on payroll taxes, the better structure for retirement contributions, the accountable plan setup, all of it stacks into something genuinely valuable over a career.

But the difference between “I have an S Corp” and “I’m using my S Corp well” is usually a tax professional who actually understands physician finances. The defaults won’t get you there. The general advice you find online won’t either.

If you’ve been running your practice or your locums work as a sole prop and your income is climbing past $200,000, this is worth a real conversation. Not a quick Google search and a DIY filing.

Talk to a tax advisor who works specifically with physicians. Get a personalized analysis of whether the numbers work for your situation. Then decide. The tax code rewards people who plan ahead, and physicians, perhaps more than anyone else, leave money on the table simply because nobody told them what was possible.

Your next move: pull last year’s tax return, look at your self-employment income, and book a consultation with a physician-focused tax strategist. That single hour might be the highest-ROI thing you do all year.

FAQs

Q: At what income level does an S Corp start making sense for a physician?

Generally, once your self-employment income hits around $80,000 to $100,000, the math starts leaning in favor of an S Corp. Below that, the costs of payroll, tax prep, and ongoing compliance can eat up the savings. For physicians clearing $200,000 or more, it’s almost a no-brainer to at least run the numbers.

Q: Can I have an S Corp if I’m also a W-2 employee at a hospital?

Yes. Plenty of physicians do exactly this. Your hospital W-2 income stays separate. The S Corp is just for your side income, locums work, consulting, telemedicine, expert witness gigs, whatever you’re doing on top. The two streams don’t interfere with each other from a structural standpoint.

Q: How much does it cost to set up and run an S Corp?

Setup is usually $500 to $1,500 depending on your state and whether you use a service or an attorney. Ongoing costs include payroll software ($600 to $1,200 a year), tax prep for the 1120-S ($1,000 to $2,500), and possibly state franchise taxes. Budget around $2,000 to $4,000 a year all-in.

Q: What happens if the IRS thinks my salary is too low?

They can reclassify your distributions as wages, then hit you with back payroll taxes, penalties, and interest. This is why documentation matters. Keep records showing how you arrived at your salary number, ideally referencing industry data like MGMA surveys or comparable W-2 positions.

Q: Can my spouse be on payroll through my S Corp?

If your spouse genuinely works in the business, yes. This can open up additional retirement contributions and other benefits. But the work has to be real and the pay has to match what you’d pay anyone else for that role. Don’t put your spouse on payroll just to shift income, the IRS sees through that.

Q: When’s the deadline to elect S Corp status?

For an existing entity, you generally need to file Form 2553 within 2 months and 15 days of the start of the tax year you want the election to take effect. So if you want it for 2026, you’d want it filed by mid-March 2026. There are late election relief provisions, but don’t rely on those.

Q: Do I lose the QBI deduction with an S Corp?

No, but it gets a bit more nuanced. As a “specified service trade or business” (which medicine is), physicians face income limits on the QBI deduction regardless of entity structure. Above certain thresholds, the deduction phases out. An S Corp doesn’t fix this, but it doesn’t make it worse either. A Physician Tax Advisor can model out how the salary/distribution split affects your QBI position.

Q: What if I want to undo my S Corp election later?

You can revoke the election, but there’s a five-year waiting period before you can re-elect S Corp status, with limited exceptions. So don’t flip back and forth casually. Make the decision deliberately.

Learn more about Physician Tax Solutions

-Our Team

-Our Process

-What we do

Visit contact physiciantaxsolutions.com to schedule a consultation and learn how we can help you take control of your tax strategy today.

This post serves solely for informational purposes and should not be construed as legal, business, or tax advice. Individuals should seek guidance from their attorney, business advisor, or tax advisor regarding the matters discussed herein. physiciantaxsolutions.com assumes no responsibility for actions taken based on the information provided in this post.

[…] The Basics of S Corps for Business Owners: A Physician’s Beginner Guide […]

[…] The Basics of S Corps for Business Owners: A Physician’s Beginner Guide […]

[…] The Basics of S Corps for Business Owners: A Physician’s Beginner Guide […]

[…] The Basics of S Corps for Business Owners: A Physician’s Beginner Guide […]

[…] The Basics of S Corps for Business Owners: A Physician’s Beginner Guide […]

[…] The Basics of S Corps for Business Owners: A Physician’s Beginner Guide […]

[…] The Basics of S Corps for Business Owners: A Physician’s Beginner Guide […]

[…] The Basics of S Corps for Business Owners: A Physician’s Beginner Guide […]

[…] The Basics of S Corps for Business Owners: A Physician’s Beginner Guide […]

[…] The Basics of S Corps for Business Owners: A Physician’s Beginner Guide […]